personal loan rejected Getting a can feel frustrating and confusing. You may have expected quick approval, especially if you needed money for an emergency, education, medical expense, home repair, or debt consolidation. But lenders do not approve loans based only on your need. They check several financial factors before deciding whether you are a safe borrower.

If your personal loan application was rejected, it does not always mean you are a bad borrower. It usually means the lender found one or more risk factors in your profile. The good news is that most of these issues can be fixed over time. Once you understand the reason for rejection, you can take steps to improve your chances next time.

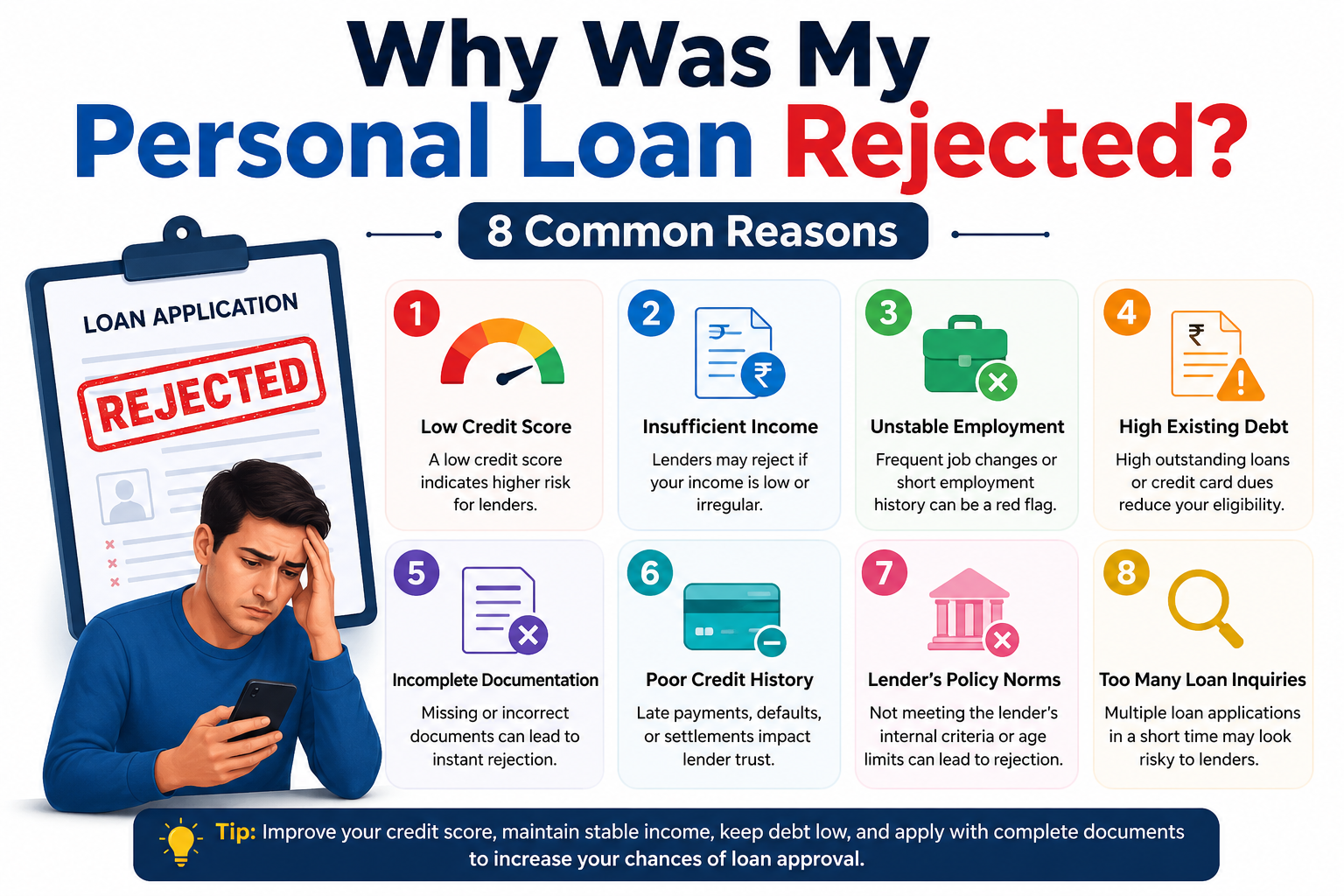

In this article, we will look at the 8 most common reasons personal loan applications get rejected and what you can do to avoid the same mistake again.

1. Low Credit Score

One of the biggest reasons for personal loan rejection is a low credit score. A credit score tells the lender how responsibly you have handled credit in the past. If your score is too low, the lender may think you are likely to miss repayments.

A poor score can happen because of late payments, credit card defaults, loan settlement, or too many unpaid dues. Even if your income is good, a weak credit score can reduce your approval chances. Lenders want to see that you have a history of paying on time.

To improve this, check your credit report regularly and fix any errors. Pay all EMIs and credit card bills on time, reduce outstanding debt, and avoid applying for too many loans at once. Over time, a better credit score can improve your loan approval chances.

2. High Debt-to-Income Ratio Personal Loan Rejected

Another common reason is a high debt-to-income ratio. This means a large part of your monthly income is already going toward existing loans, EMIs, or credit card payments. If too much of your salary is already committed, the lender may feel you cannot handle another loan.

Even if you earn a decent income, heavy debt can make your profile risky. For example, if you already pay multiple EMIs every month, a new personal loan may stretch your budget too far. Lenders want to see that you still have enough income left after paying your current obligations.

To improve this, try reducing existing debts before applying again. You can also close small loans, pay down credit card balances, or apply for a smaller loan amount. A lower debt burden makes you look more financially stable.

How to Get a Personal Loan Approved in 24 Hours in the USA

3. Insufficient or Unstable Income

Personal loan lenders usually want to see a steady source of income. If your income is too low or unstable, they may reject the application. This is because the lender needs confidence that you can repay the monthly EMI without difficulty.

Freelancers, self-employed people, or applicants with irregular income may face more scrutiny. If your salary is not consistent or your bank statements do not show regular cash flow, the lender may consider your income uncertain. Even if you earn well in some months, inconsistency can still be a problem.

To improve your chances, show clear proof of income such as salary slips, bank statements, income tax returns, or business records. If possible, apply after building a stronger income history. You can also choose a loan amount that matches your repayment capacity.

4. Poor Employment History Personal Loan Rejected

Job stability matters a lot in personal loan approval. If you have recently changed jobs too often, have short employment history, or are in a probation period, lenders may see you as higher risk. A stable job usually gives lenders more confidence in your repayment ability.

This is especially important for salaried applicants. A lender may prefer someone who has been working with the same employer or in the same field for a reasonable period. Frequent job changes can make your income appear less secure, even if your salary is good.

To improve this, wait until you have a more stable work record before applying. If you are switching careers or working on contracts, provide as much documentation as possible. A stronger employment profile can improve trust.

5. Incomplete or Wrong Documents

Many personal loan applications get rejected because of simple document issues. Missing documents, mismatched details, incorrect PAN or ID information, wrong address proof, or incomplete application forms can all lead to rejection. Sometimes the lender is ready to approve the loan, but the paperwork creates a problem.

This happens more often than people think. Even a small mistake in your name, date of birth, address, or bank details can cause delays or rejection. If the documents do not match across records, the lender may ask for clarification or decline the application.

To avoid this, double-check every document before submitting. Make sure your details match across your ID, bank account, income proof, and application form. Keep scanned copies ready and use only updated documents.

6. Too Many Loan Applications

Applying for too many loans in a short time can hurt your chances. Every time you apply, the lender may check your credit report. Too many hard inquiries can make you look desperate for credit or financially stressed.

Lenders may assume that if several institutions have already rejected you, there may be a hidden risk. This can lower their confidence and reduce the chance of approval. A long list of recent applications can also affect your credit profile.

The better approach is to apply only where you meet the eligibility criteria. Compare lenders first, then choose the most suitable one. Avoid sending multiple applications at the same time unless necessary.

7. High Existing Credit Card Usage

Even if you pay your credit card bills on time, using too much of your credit limit can still be a problem. Lenders may see high credit card usage as a sign that you depend heavily on borrowed money. If your cards are regularly maxed out, it may suggest financial pressure.

High utilization can lower your credit score too. Most experts suggest keeping credit card usage well below the limit. If you consistently use most of your available credit, lenders may think adding another loan would be risky.

To fix this, try lowering your credit card balances before applying. Pay more than the minimum due and avoid carrying large revolving balances. A healthier credit card profile can support your loan request.

8. Lender Eligibility Not Met

Every lender has its own rules. Some require a minimum monthly income, specific job type, a certain age range, or a particular credit score. If you do not meet even one of these requirements, your loan can be rejected immediately.

This is one of the easiest reasons to overlook because many applicants apply first and check eligibility later. But lenders are strict about their criteria. What works for one bank or fintech company may not work for another.

To avoid this, always read the eligibility rules before applying. Check whether the lender accepts your employment type, income level, credit score, and location. Choosing the right lender can make a big difference.

How to Improve Approval

If your personal loan was rejected, do not panic. A rejection today does not mean rejection forever. The first step is to understand the likely reason and improve your profile before applying again. Small changes can make a big difference.

Here are a few simple actions that help:

- Pay all EMIs and bills on time.

- Reduce existing debt before reapplying.

- Keep your credit card usage low.

- Maintain stable income and employment records.

- Submit complete and correct documents.

- Apply only to lenders whose rules you meet.

It is also smart to wait a little before reapplying, especially if the rejection was due to a low credit score or too many recent applications. Use that time to strengthen your financial profile instead of rushing into another rejection.

Final Thoughts

A personal loan rejection is not the end of the road. In most cases, it is a signal that something in your financial profile needs attention. Whether the issue is a low credit score, high debt, unstable income, or missing documents, you can usually fix it with time and discipline.

The key is to apply strategically, not randomly. When you understand how lenders evaluate risk, you can prepare a stronger application and improve your chances of approval. A well-planned application is much more likely to succeed than a rushed one.

Suggested FAQ

Why was my personal loan rejected even with a good salary?

Because lenders also check credit score, debt load, job stability, and documents, not just income.

Can I apply again after rejection?

Yes, but it is better to fix the reason first before reapplying.

Does loan rejection affect credit score?

A single rejection usually does not hurt much, but too many applications can affect your credit profile.

What is the most common reason for loan rejection?

Low credit score and high debt are among the most common reasons.

Apply here: Check your personal loan eligibility and apply online